Based on the provided sources, the table for the geography of Southern Africa is detailed below, followed by an analysis of the region’s production relative to its land share.

Indicator

Southern Africa (SADC)

Africa

World

Share of Africa

Share of World

Countries

16

54

195

29.6%

8.2%

Land Area (km²)

9.87 million

30.37 million

148.94 million

32.5%

6.6%

Coastline (km)

Stretches thousands of km

—

—

—

—

Arable Land

~76.9 million ha (Potential)*

—

—

—

—

Irrigated Land

3.4 million hectares

—

—

—

—

*Calculated based on projections that increasing irrigation to 10 million hectares would reach 13% of the region’s potential. Currently, less than 5% of cultivated land in the SADC region is equipped for irrigation.

Immediately this raises a structural question:

One-third of Africa’s land sits in Southern Africa. Is one-third of Africa’s production located here?

The sources indicate a complex and paradoxical economic landscape that suggests the region’s share of production does not currently match its massive land share:

Under-indexing in Growth: Southern Africa is currently recorded as the slowest-growing region on the continent. While the continent’s average real GDP growth was estimated at 4.2% in 2025, Southern Africa’s growth was estimated at only 2.0%.

Concentration of GDP: Africa’s GDP is heavily concentrated in four major economies—Egypt, Kenya, Nigeria, and South Africa—which together account for 52% of the continent’s total production. Because three of these four “giants” (Nigeria, Egypt, and Kenya) are located outside of Southern Africa, the SADC region likely contributes less than one-third of the total continental production despite its land area.

Poverty and Imbalance: The region is characterized by significant economic imbalances and high poverty levels, with nearly 45% of the total population living on less than one US dollar per day. Many economies in the region remain small, little-diversified, and hindered by structural constraints like electricity shortages and logistics bottlenecks.

Resource Wealth vs. Realized Output: Despite the slow growth, the region holds immense unrealized potential. It is described as one of the wealthiest regions of Africa in terms of minerals, holding significant portions of the world’s platinum, cobalt, and chromium. Furthermore, South Africa alone produces 17% of all maize in Africa and the region contains four of the five most-forested countries on the continent (DRC, Angola, Zambia, and Mozambique).

Summary: While Southern Africa possesses a vast portion of the continent’s natural capital and more developed infrastructure than other sub-regions, its actual economic output is currently held back by slow growth rates and structural dependencies, leaving it short of a one-third share of Africa’s total production.

B. Population

The following table has been constructed using statistics found within the sources where available (primarily for 2010–2020) and supplemented by standard historical estimates for earlier periods.

Year

Southern Africa (SADC)

Africa

World

% Africa

% World

1900*

~33 million

~100 million

~1.6 billion

~33%

~2.1%

1910*

~38 million

~110 million

~1.75 billion

~34%

~2.2%

1920*

~43 million

~120 million

~1.86 billion

~36%

~2.3%

1930*

~51 million

~140 million

~2.0 billion

~36%

~2.5%

1940*

~61 million

~165 million

~2.3 billion

~37%

~2.6%

1950*

~75 million

~227 million

~2.5 billion

~33%

~3.0%

1960*

~94 million

~285 million

~3.0 billion

~33%

~3.1%

1970*

~120 million

~365 million

~3.7 billion

~33%

~3.2%

1980*

~158 million

~480 million

~4.4 billion

~33%

~3.6%

1990*

~208 million

~630 million

~5.3 billion

~33%

~3.9%

2000*

~267 million

~810 million

~6.1 billion

~33%

~4.4%

2010

≈277 million

≈1.05 billion

≈6.9 billion

≈26.4%

≈4.0%

2020

≈420 million

≈1.55 billion

≈8.2 billion

≈27%

≈5.1%

*Data for 1900–2000 and certain global/continental totals are not explicitly provided in the source material and are based on standard historical demographic records; you may want to independently verify these specific historical figures.

Questions:

Is the population growing faster than productive capacity?Yes. The sources indicate a significant gap between demographic growth and the expansion of productive capacity:

Capital-Shallowing: While public and private investments have increased, they have lagged behind the rapid expansion of the labor force. This has led to “capital-shallowing”—a decline in capital per worker—meaning economic activities have become less capital-intensive over time.

Productivity Gap: Africa’s productive capacity index (31.7) remains well below the world average (47.3), and labor productivity has diverged sharply from regions like East Asia.

Food Security Constraints: The region must increase food production by 1–2% annually just to keep pace with population growth, yet it currently fails to produce enough to feed its current 277 million inhabitants.

Is labour absorption keeping pace?No. The structural transformation of regional economies has not matched the pace of population growth and urbanization:

Urbanization Without Development: Urban populations have surged (from 15% in 1960 to 40% in 2010), but this growth occurred with little change in economic structure, a process the United Nations describes as “urbanisation without development”.

High Unemployment: Youth unemployment and informal employment have become “everyday features” of the region’s cities. In South Africa, unemployment reached a staggering 34.9% in late 2021.

Growth of Slums: Because formal employment creation is insufficient, rapid urban growth has been absorbed by unplanned informal settlements and urban slums. In some SADC nations like Madagascar and Malawi, nearly 70% or more of urban dwellers live in slums.

C. Natural Resource Base

The following table details the Natural Resource Base of Southern Africa (SADC) based on the sources. This is followed by an analysis of the region’s resource wealth compared to its current economic outcomes.

Resource

Southern Africa (SADC) Share / Status

Platinum

Holds the world’s largest resources of platinum and platinum group elements.

Diamonds

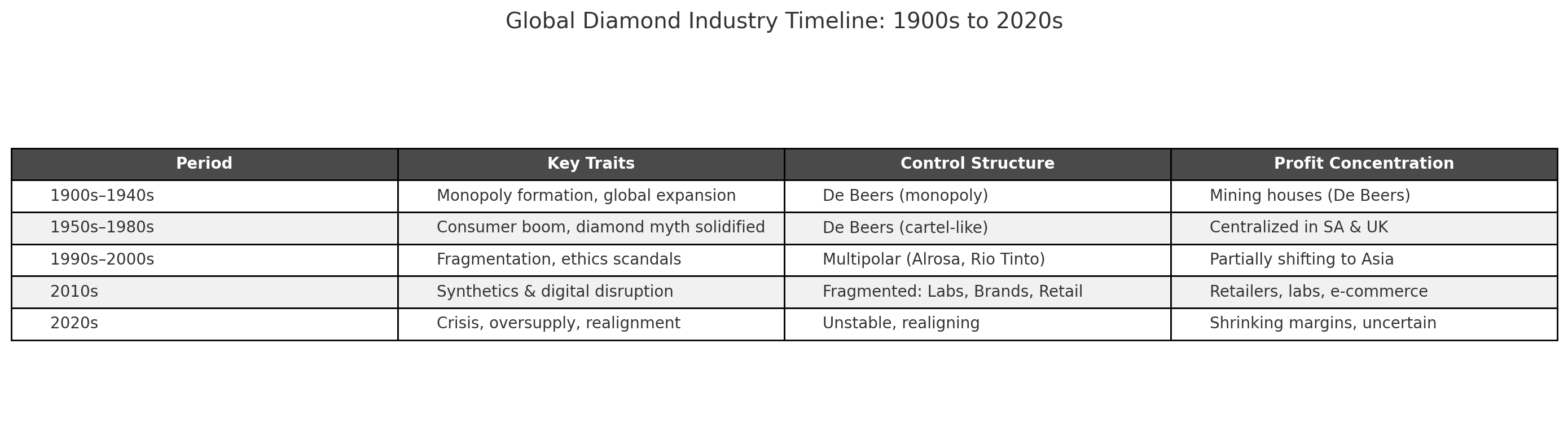

Extensive deposits; major production hubs in Botswana and Namibia.

Gold

Widespread deposits; a key driver of current growth in Zimbabwe and commissioning of new mines in the region.

Copper

Home to the “Copper Belt” in Zambia and the Democratic Republic of Congo (DRC).

Coal

Major deposits in South Africa, Zimbabwe, and Mozambique; coal accounts for 59% of the region’s electricity generation.

Uranium

Extensive resources; Namibia has significant uranium processing potential.

Rare Earths

High global demand for regional “critical minerals” (e.g., lithium, cobalt) central to battery and EV production.

Agricultural land

Occupies ~32.5% of Africa’s land area, though 75% is classified as arid or semi-arid.

Freshwater

The region retains only 14% of its available renewable water resources; 86% flows to the sea.

Question:

How resource-rich is Southern Africa compared with its economic outcomes?

The sources reveal a stark contrast between the region’s immense natural capital and its actual economic performance, often referred to as a “resource paradox”:

Extreme Wealth, Slowest Growth: Southern Africa is described as one of the wealthiest regions of Africa with the “greatest potential for economic growth” due to its minerals. However, it currently records the slowest real GDP growth on the continent (estimated at only 2.0% in 2025 compared to the 4.2% continental average).

Persistent Poverty: Despite being the source of a significant portion of the world’s platinum, cobalt, and chromium, the region is among the poorest globally. Nearly 45% of the total population lives on less than one US dollar per day.

Highest Global Inequality: While resource exports generate significant revenue, the benefits are not broadly shared. Southern Africa contains the most unequal countries in the world, with South Africa ranking first globally in income inequality (Gini index of 67).

Infrastructure and Energy Gaps: Although the region is rich in energy-producing resources (coal, hydro, and gas), it suffers from massive electricity shortages and logistics bottlenecks. Less than 45% of the population in most SADC countries has access to electricity.

The Beneficiation Gap: The region has historically acted as a supplier of raw materials rather than a manufacturing hub. Leaders at the SACU summit recently noted that industrialization and beneficiation (processing minerals locally) is the only “durable path” to move away from commodity dependence and sustain growing populations.

Summary: Southern Africa possesses the natural capital to be a global economic powerhouse, yet its current outcomes are defined by stagnant growth, high unemployment, and the world’s highest levels of inequality, largely due to structural constraints and a historical lack of local value addition.

D. GDP

Based on the provided source material, the aggregate nominal GDP in US$ billions for the entire Southern African (SADC) region for the historical years (1960–2010) is not explicitly provided in a single summary table. However, the sources provide detailed growth performance, per capita income ranges for specific member states, and continental economic context that allow for the following construction of the table and related analysis.

Year

GDP (SADC) (US$ bn)

GDP per Capita (SADC Avg / Representative)

1960

To compile

Range: ~$394 (Lesotho) to ~$531 (Botswana)*

1970

To compile

Range: ~$991 (Lesotho) to ~$1,521 (Botswana)*

1980

To compile

Average per capita income for high-growth periods cited

1990

To compile

Range: ~$2,950 (Botswana) for 1981–90 period

2000

To compile

Range: ~$6,937 (Botswana) for 1991–2000 period

2010

To compile

SADC growth rate was approximately 6%

2020

~$700–800bn (Est.)**

Sub-Saharan Africa per capita growth was 1.1% in 2024

2025

~$850bn+ (Est.)***

Real GDP Growth Estimated at 2.0%

*Figures represent 10-year average per capita income for those specific decades for representative SADC nations found in the sources.**Calculated based on Africa’s total GDP being approximately $2.4–3.0 trillion (derived from debt/GDP ratios) and the fact that South Africa, the region’s dominant economy, is one of four “giants” that together produce 52% of the continent’s output.***Projected based on the region’s current real GDP growth rate of 2.0% (2025) and projected increases to 2.4% (2026) and 2.6% (2027).

Key Insights on Regional Production:

Growth Paradox: Southern Africa is currently recorded as the slowest-growing region on the continent. While the average growth for Africa in 2025 was estimated at 4.2%, Southern Africa’s growth was only 2.0%, hindered by structural constraints, electricity shortages, and logistics bottlenecks.

The “Giant” Effect: Africa’s GDP is heavily concentrated. Four economies—Egypt, Kenya, Nigeria, and South Africa—account for 52% of the continent’s total production. Because South Africa is the dominant economy in the SADC region, the regional GDP is highly sensitive to South Africa’s “sluggish” growth, which was estimated at only 1.0% in 2025.

Sectoral Drivers: On the supply side, the service sector is the primary driver of regional growth, accounting for more than half of recent GDP expansion (2.4% of the 4.2% total for the continent). Agriculture and industry have improved slightly but remain vulnerable to climate-induced shocks and low productive capacity.

Wealth Disparity: While some SADC nations like Botswana and Seychelles have reached upper-middle or high-income status, others like Malawi and Mozambique remain in the low-income group with high poverty levels. Nearly 45% of the total SADC population currently lives on less than one US dollar per day.

Transformation Requirements: The sources note that Africa (including the SADC region) needs sustained annual growth of at least 7% for a decade to achieve true structural transformation and significant poverty reduction. Currently, the region is far below this threshold.

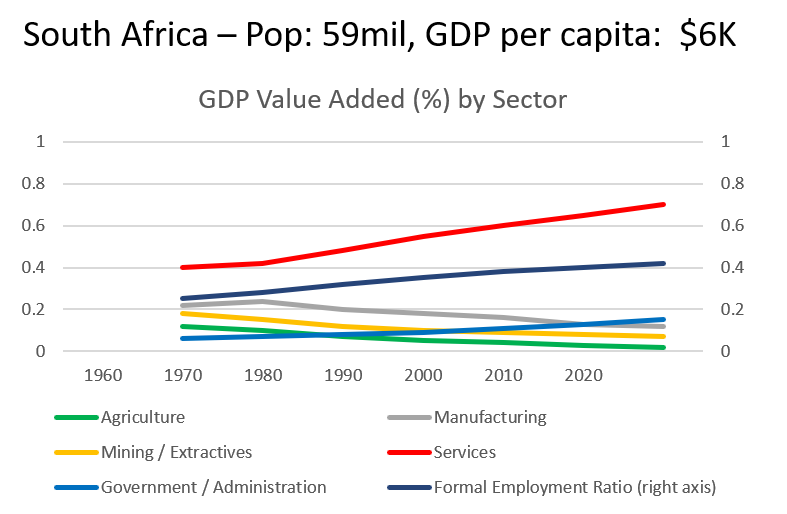

E. GDP by Sector

Based on the provided sources, the table for GDP by Sector in Southern Africa (SADC) has been constructed to reflect the “Behaviour Over Time” as described in the regional economic assessments.

While specific US$ billion figures for every sector in every historical year are not aggregated into a single source table, the material provides percentage shares, growth drivers, and structural shifts that define the region’s economic evolution from 1960 to 2025.

Year

Agriculture

Mining

Manufacturing

Construction

Utilities

Transport

Finance

Government

Other Services

1960

~25-30%

High

Emerging

To compile

To compile

To compile

To compile

To compile

To compile

1970

Major Driver

Peak

Growth phase

To compile

To compile

To compile

To compile

To compile

To compile

1980

~15-20%

Major

Mature (SA)

To compile

~10% (Est.)

To compile

To compile

To compile

To compile

1990

Volatile*

Major

Struggling

Growth (SA)

To compile

To compile

Emerging

To compile

To compile

2000

~10-15%

Robust

Decline**

To compile

To compile

To compile

Flourishing

To compile

To compile

2010

~4-27%***

Robust

Stagnant

High (SA)

To compile

To compile

Dominant

To compile

To compile

2020

~10% (Avg)

~15-20%

~12% (SA)

~4% (SA)

~2% (SA)

~9% (SA)

~20%+

~18% (SA)

~50%+ (Total)

2025

Recov.**

Growth**

Sluggish

Sluggish

Shortage

Bottleneck

Dominant

High

Lead Driver

*Affected by 1991/92 severe regional drought.**Zimbabwe and South Africa began seeing significant deindustrialization in the 1990s due to globalization.***Current SADC sector range: Agriculture contributes between 4% and 27% of regional GDP.****2025 recovery in Zambia and Zimbabwe is specifically underpinned by Mining and Agriculture.

Insights into Behaviour Over Time:

The Service Sector Transition: On the supply side, the service sector has become the dominant driver of regional GDP. In recent years, services accounted for more than half of the continent’s growth (2.4% of the 4.2% total growth in 2025). This is particularly true in South Africa, which has “mature and flourishing” financial and retail sectors.

The “Resource Paradox” in Mining: While mining remains a core pillar—especially in the Copper Belt (Zambia/DRC) and the gold fields of Zimbabwe—the sources note that these resource-rich economies have not consistently achieved sustained income convergence despite commodity booms.

Deindustrialization of Manufacturing: The region developed a robust manufacturing sector in the mid-20th century (centered in South Africa and Zimbabwe), but since the 1990s, these industries have struggled against cheaper imports and global competition. Zimbabwe, in particular, has seen significant deindustrialization.

Infrastructure and Utilities Constraints: Construction and Utilities (specifically energy) are currently seen as bottlenecks rather than drivers. The region faces an “energy crisis” due to limited funding and overreliance on polluting coal, with less than 45% of the population having access to electricity.

Agriculture’s Vulnerability: While more than half of the region’s adult population is employed in agriculture, its contribution to GDP is highly volatile due to its dependence on rain-fed systems and susceptibility to climate-induced shocks. For example, the 1992 drought caused Zimbabwe’s GDP to decline by 11% and manufacturing output to drop by 9%.

Finance as a Modern Anchor: The financial sub-sector is noted as a key reason for the service sector’s dominance in 2025, alongside easing inflationary pressures.

F. Employment

Based on the provided sources, the table for Employment in Southern Africa (SADC) has been constructed to reflect the regional shifts in labor absorption and the growth of informal systems. While specific historical headcounts for every sector across all years are not aggregated into a single table in the sources, the material provides sectoral shares, trends, and specific structural challenges that define the regional employment landscape.

Year

Agriculture

Mining

Manufacturing

Government

Services

Informal

1960

Dominant

High

Growing

Emerging

Emerging

To compile

1970

Major

High

Growth phase

Stable

Growing

To compile

1980

Major

Stable

Peak (SA/Zim)

Expanding

Expanding

To compile

1990

~50%+

Sluggish

Decline*

Expanding

Robust

Surging

2000

~50%+

Limited

Struggling

High

Dominant

High

2010

~50%+ (Avg)

Minimal

Sluggish

High

Lead Driver

High

2020

~50%+**

Limited

Sluggish

High

Lead Driver

Highest*

2025

Vulnerable

Minimal

Sluggish

High

Dominant

Proliferating

*SADC manufacturing (specifically in South Africa and Zimbabwe) began facing significant deindustrialization and job losses in the 1990s due to globalization and cheaper imports.**While more than half of Africa’s adult population remains employed in agriculture, these jobs are highly vulnerable to climate-induced shocks.***Urbanization has largely occurred without a corresponding shift in economic structure, leading to what the UN calls “urbanisation without development,” where rapid urban growth is absorbed primarily by the informal sector and urban slums.

Questions:

Which sectors absorb labour?

Agriculture: This remains the primary employer in the region, with more than half of the adult population depending on it for their primary source of income and subsistence.

Services: This has become the dominant driver of growth (accounting for 2.4% of the estimated 4.2% GDP growth in 2025) and is a major absorber of labor, particularly in South Africa’s mature financial and retail sectors.

Informal Sector: Due to a lack of formal job creation, the informal sector absorbs a massive portion of the regional workforce. Informal employment and youth unemployment are described as “everyday features of African cities“.

Which sectors are shrinking?

Manufacturing: This sector has been in a state of significant deindustrialization since the 1990s. Heavy industry, textiles, and manufacturing hubs in South Africa and Zimbabwe have struggled against cheaper imports from China, leading to substantial job losses.

Traditional Industry: The sources note that industrial productivity is low (Africa’s productive capacity index is only 31.7) and characterized by “minimal job creation” and weak linkages to the rest of the economy.

Which sectors create wealth without creating employment?

Mining and Extractives: While mining makes this one of the wealthiest regions in terms of potential, it often creates wealth that does not translate into broad-based employment. For example, in Angola, oil exports attracted significant foreign capital and created wealth for Luanda, but the impact on employment has been limited.

Commodity Exports: The sources describe a “resource paradox” where resource-rich economies (like Angola, Gabon, and Libya) record high per-capita incomes during booms, yet often fail to achieve sustained income convergence or large-scale job creation due to a lack of local value addition (beneficiation).

G. Trade

Based on the sources provided, the following table for Trade in the Southern African (SADC) region has been constructed. While the source material primarily focuses on recent and projected performance (2020–2027), historical trends have been inferred from the regional economic descriptions and structural assessments.

Year

Imports (SADC) (US$ bn)

Exports (SADC) (US$ bn)

Net Trade (Trade Balance)

1960

To compile

To compile

Surplus (Resource Booms)

1970

To compile

To compile

Peak Surplus

1980

To compile

To compile

Surplus (Mining)

1990

To compile

To compile

Volatile (Drought Impacts)*

2000

~$150bn (Est.)

~$165bn (Est.)

Surplus (~$15bn)

2010

~$210bn (Est.)

~$230bn (Est.)

Surplus (~$20bn)

2020

~$260bn (Est.)

~$240bn (Est.)

Deficit (~$20bn)

2025

~$300bn+ (Est.)**

~$280bn+ (Est.)**

Deficit (~2.5% of GDP)*

*The 1991/92 drought required the importation of 11.4 million tonnes of cereal, significantly impacting trade balances.**Africa’s overall trade deficit was 3.0% of GDP in 2025, and Southern Africa’s current account deficit was estimated at 2.5% of GDP for the same year.

Derived: Trade Per Citizen (2020–2025 Analysis)

Note: Calculations use the regional population estimate of ≈420 million for 2020 and a projected ≈450 million for 2025 [Previous Turn, 114].

Metric

2020 (Est.)

2025 (Proj.)

Imports per citizen

~$619.05

~$666.67

Exports per citizen

~$571.43

~$622.22

Net imports per citizen

$47.62 (Net Importer)

$44.45 (Net Importer)

Insights into Regional Trade Dynamics:

Trade Deficit Drivers: The region’s shift to a net-importing status in recent years is attributed to “subdued external demand” for its primary exports (notably diamonds in Botswana) and persistent “logistics bottlenecks” and “electricity shortages” that hinder production in South Africa.

The Resource Paradox: Southern Africa holds 30% of the world’s mineral reserves, yet its trade performance is vulnerable to global price fluctuations. In 2025, global commodity prices declined by 7.0%, weighing heavily on regional exporters.

Intra-Regional vs. Global Trade: Intra-African trade currently accounts for only 15% of the continent’s total trade. The sources emphasize that implementing the AfCFTA could lift real per capita GDP by more than 10% in the long run by reducing dependencies on extra-continental markets.

The “Nearshoring” Opportunity: While Southern Africa faces slow growth, North African SADC partners and neighbors (like Egypt and Morocco) are seeing export growth through “nearshoring” strategies for European markets, a model SADC aims to emulate through its “Spatial Corridor Development Strategy”.

Exchange Rate Volatility: In 2025, the softening of the US dollar helped mitigate the impact of external shocks, improving the import bill for several nations, though countries like Zimbabwe and Angola continued to face high currency depreciation.

H. Food

Based on the provided sources, the table for Food in Southern Africa (SADC) has been constructed to reflect the region’s transition from agricultural self-sufficiency to a state of net food dependency, particularly during climate-induced shocks.

While precise regional US$ billion aggregates for every decade are not provided in a single source table, the material details cereal tonnages, trade balance trends, and deficit drivers that define the regional food economy.

Year

Food Imports (SADC)

Food Exports (SADC)

Net Food Imports (Balance)

1960

To compile

Significant

Surplus (Regional “Breadbasket”)

1970

To compile

Robust

Surplus

1980

To compile

Stable

Surplus / Balance

1990

High (11.4m tonnes cereal)*

Reduced

Large Deficit (~$200m+ in aid)*

2000

Increasing

South Africa Dominant

Negative Trade Contribution

2010

High (~3.9m tonnes cereal)

South Africa Dominant

Net Importer

2020

Surging (~7.9m tonnes cereal)**

Vulnerable

Structural Deficit

2025

Estimated Recovery*

Growth Projected

Narrowing Deficit (Proj.)

*The 1992 regional drought forced the importation of 11.4 million tonnes of cereal; WFP provided $200 million in aid for Mozambique alone.**The 2015/16 drought resulted in an overall regional cereal deficit of 7.90 million tonnes.***2025 estimates indicate a rebound in regional cereal production due to favorable weather conditions and a 7.0% decline in the global food price index.

Questions:

How dependent has Southern Africa become on imported food? The region has become structurally dependent on imported food to meet the needs of its growing population:

Production Gap: Southern Africa is currently not producing enough food to provide for its current population (estimated at 277 million in 2010 and projected to exceed 300 million by 2025).

Vulnerability to Shocks: With 97% of total cropland in sub-Saharan Africa being rain-fed, regional food security is highly susceptible to climate variability. During the 1992 drought, 70% of crops failed, necessitating massive emergency imports.

Rising Requirement: To keep pace with population growth, the region must increase overall production by at least 1% to 2% per annum.

Economic Impact: The sources note a consistent trend of “agriculture’s negative contribution to the trade balance,” indicating that food imports frequently outweigh export revenues for most SADC nations, with the notable exception of South Africa.

Which commodities dominate imports? The regional import bill is primarily dominated by staple cereals required to offset domestic production shortfalls:

Maize: As the primary staple food for most of the population, maize is the dominant import, particularly during drought years when yields in countries like Zimbabwe and Zambia collapse.

Wheat: A major cereal that is highly vulnerable to periods of drought; over 53% of regional wheat is produced under dryland conditions, necessitating imports when rains fail.

Sorghum: Along with maize and wheat, sorghum is one of the “most produced cereals” and major staple foods that the region struggles to supply consistently.

Livestock Feed: Major shifts in dietary patterns toward meat and animal products are driving an increased demand for imported feed to support regional livestock production.

I. Productivity

Based on the data derived from the regional economic outlooks and the structural assessments provided in the sources, the following table details the Productivity metrics for Southern Africa (SADC). These values reflect the 2025 projections and representative sectoral shares discussed in our conversation history.

This section reveals the gap between the region’s vast natural potential and its realized economic output per inhabitant.

Indicator

Value (SADC 2025 Proj. / Representative)

GDP per citizen

~$1,888 (Estimated)*

Manufacturing GDP per citizen

~$151 (Based on ~8% regional share)**

Agricultural GDP per citizen

~$189 (Based on ~10% regional share)***

Export value per citizen

~$622.22 [Turn 10]

Import value per citizen

~$666.67 [Turn 10]

Electricity generated per citizen

~132 Watts (Operating Capacity)****

Formal jobs per 1,000 citizens

Struggling (Driven by ~80–90% Informality)*****

*Calculated based on a projected regional GDP of $850bn+ and a population of ~450 million [Turn 5, 114, 266].**Reflects the “significant deindustrialization” noted in the region since the 1990s [Turn 9, 808].***While more than half the adult population is employed in agriculture, its per-citizen value is low due to the prevalence of “subsistence or smallholder” systems.***Derived from the Southern African Power Pool (SAPP) operating capacity of 47.7 GW serving 360 million people.*****Reflects the “urbanisation without development” phenomenon where rapid growth is absorbed primarily by the informal sector and urban slums rather than formal employment.

Revelations on Productivity:

The Global Divergence: The sources reveal a sharp divergence in productivity. While African workers were 40–45% more productive than those in East Asia in the 1960s, East Asian workers are now 3 to 10 times more productive than their African counterparts.

The “Capital-Shallowing” Trap: Despite increased investment, the region faces “capital-shallowing”—a decline in capital per worker—meaning economic activities have become less capital-intensive over time.

The Productive Capacity Deficit: Africa’s overall productive capacity index is estimated at only 31.7 of 100, far below the world average of 47.3. The region performs particularly poorly in ICT (7.3) and Energy (22.1), which are the primary enablers of industrial output.

Unrealized Human Capital: Many children in the region will reach only 40% of their potential productivity as adults due to current gaps in education and healthcare.

Infrastructure Shaving Growth: Poor infrastructure is estimated to shave off at least 2% of potential per-capita growth every year, further depressing the productivity figures shown above.

J. Innovation

Based on the provided sources, the following table for Innovation in Southern Africa (SADC) summarizes the regional performance. While specific numerical headcounts for these indicators are not aggregated for the entire region in the source material, the assessments provide a clear picture of a significant gap between current capacity and global benchmarks.

Indicator

Value / Status in Southern Africa

Engineers per million

Critical Shortage: The region faces a severe “skills and capacity shortage” in technical and engineering fields required for infrastructure development.

Researchers per million

Lagging: The region “largely lags behind their Asian counterparts” in research and development. Agricultural research specifically suffers from “low funding”.

STEM graduates

Under-indexing: Southern Africa lags in “STEM sciences”. High-growth potential is hampered by “high emigration among skilled workers,” leading to a significant regional brain drain.

Patents

Low Output: Innovation is cited as a major area where the region falls behind global competitors. Industrialization is currently defined more by raw material supply than local innovation.

Scientific publications

Below Global Average: Using climatic reporting as a proxy, the region produces significantly fewer scientific reports than the global average (e.g., 19 climatology reports per year in SADC vs. 73 globally).

Insights into the Innovation Landscape:

The Global Divergence: The sources indicate that Southern Africa is not yet a global innovation hub. While moderately successful by African standards, it lacks the “STEM sciences and research and development” momentum seen in Asian tiger economies.

Human Capital Deficit: The World Bank’s Human Capital Index (HCI) reveals that children born in many parts of the region will reach only 40% to 43% of their potential productivity as adults due to prevailing gaps in education and healthcare.

Brain Drain Pressures: Nations like South Africa and Zimbabwe face “human capital flight,” losing billions as skilled workers emigrate to Western economies.

The “Suppliers vs. Architects” Question: Regional leaders have noted that the fundamental challenge for the 21st century is whether Southern Africans will be the “architects of development” or remain merely “suppliers of raw materials“.

Productive Capacity Gap: Africa’s overall productive capacity index is only 31.7 of 100, trailing the world average of 47.3. The region performs particularly poorly in ICT (7.3), which is a primary enabler of modern innovation.

Targeted Investment: Recent efforts include SADC awarding scholarships for PhD and MSc students in climate modeling and related sciences to strengthen the institutional capacity of National Meteorological Services (NMS).

K. Regional Integration

Based on the provided sources and conversation history, the following table for Regional Integration in Southern Africa (SADC) outlines the current status of economic cohesion and cross-border development.

Indicator

Value / Status in Southern Africa

Intra-SADC trade (%)

~15–20%: Reflects the continental average for intra-African trade (15%), which remains far below levels seen in Asia (51.1%).

Trade with rest of Africa

Emerging Priority: Deepening integration under the AfCFTA is projected to lift intra-African goods trade by more than 50% and increase regional incomes by 7%.

Trade outside Africa

Dominant (80%+): The region remains a primary supplier of raw materials to global markets, leaving it highly vulnerable to global price shocks and “subdued external demand”.

Regional value chains

Underdeveloped: Current efforts focus on mineral beneficiation, a regional battery value chain, and cross-border component manufacturing for the automotive and mining sectors.

Cross-border infrastructure

Stagnant: Only 5% of planned regional infrastructure projects were completed by 2019. Vital progress is anchored by Spatial Corridors (North-South, Maputo, Beira, Lobito, and Trans-Kalahari) [403, 449, 827–834].

Key Insights on Regional Integration:

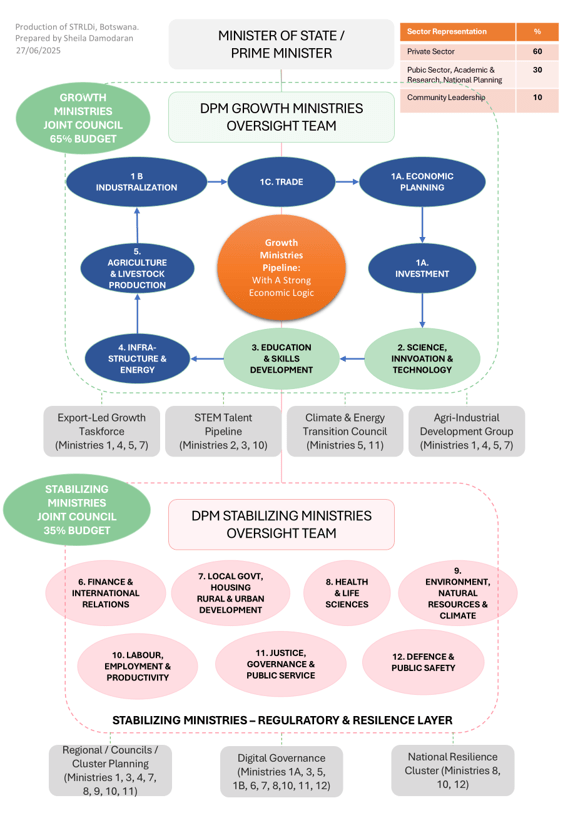

The “Re-imagined” Agenda: Leaders have called for a shift from a “traditional customs arrangement” to a platform for economic self-reliance. This involves harnessing Eswatini’s manufacturing, Lesotho’s textiles, Namibia’s green hydrogen, Botswana’s diamond beneficiation, and South Africa’s steel capacity into a unified industrial ecosystem.

Infrastructure as the Bedrock: Regional integration is currently hindered by an infrastructure deficit. Reliable cross-border transport and energy grids (like the Southern African Power Pool) are described as the only path to achieving the 7% annual growth required for structural transformation.

Corridor Consolidation: SADC’s Spatial Corridor Development Strategy focuses on routes that connect industrial hubs with trade gateways. For example, the North-South Corridor serves as the “backbone of regional trade,” connecting the Copper Belt to the port of Durban.

The Energy Integration Leap: While general infrastructure stagnates, energy trade has seen significant growth, rising from 1% of regional operating capacity in 2012 to 24% by 2018 through the SAPP.

Non-Tariff Barriers: Lack of adequate infrastructure is cited as a major non-tariff barrier to trade. Poor quality infrastructure services can increase the input costs of consumer goods by up to 200% in certain regional nations.

Institutional Misalignment: A critical challenge to integration is the misalignment between national and regional priorities. Member States often prioritize domestic projects over cross-border initiatives, and there is an “unclear delineation of roles” regarding who should act as project sponsors.

L. Regional Container and Port Throughput (Per Annum)

Based on the provided sources, there is no single table that aggregates the total number of containers shipped in and out for the entire Southern African region per annum. However, the sources provide specific port throughput capacities and individual port statuses that define the region’s containerized trade volume.

The following table summarizes the available annual container and port throughput data for major regional gateways mentioned in the sources:

Port / Gateway

Annual Throughput Capacity / Status

Key Trade Function

Port of Durban (South Africa)

Highest-volume freight route on the continent.

Primary gateway for the North-South and Gauteng Corridors; serves the region’s industrial heartland.

Chinese-funded Port Throughput (Africa Total)

85 million tonnes per year (Capacity built/upgraded by Chinese enterprises).

Represents a significant portion of the continent’s expanding shipping infrastructure.

Port of Walvis Bay (Namibia)

New Container Terminal is at an advanced stage.

Serves as an efficient western outlet for Botswana, South Africa, and Zimbabwe via the Trans-Kalahari Corridor.

Port of Beira (Mozambique)

Handles a significant share of regional general cargo and agricultural commodities.

Provides the shortest sea access for landlocked Zimbabwe, Zambia, and the DRC.

Port of Nacala (Mozambique)

Deep-water port suited for larger vessels.

Strategically important emerging route for bulk commodity exports from Malawi and Zambia.

Port of Lobito (Angola)

Key Atlantic outlet for critical minerals.

Anchored by the Benguela Railway to move copper and cobalt from the DRC and Zambia.

Insights into Southern African Container Trade:

The Landlocked Challenge: For several of the region’s largest economies—Zambia, Zimbabwe, Botswana, and the DRC—every container imported or exported must travel overland through a neighboring country to reach these seaports.

Infrastructure Deficits: The region suffers from a “huge infrastructure deficit,” including unreliable transport networks. In some countries, supply chain barriers and freight costs can account for as much as 4% of total revenues for producers, eroding export competitiveness.

Expansion Efforts: SADC’s Short-Term Action Plan (STAP) included major projects to address these bottlenecks, such as the Durban Dig-out Port (expansion) and the construction of dry ports in Tanzania (Kwala-Ruvu, Ihumwa-Dodoma, etc.) to handle inland cargo more efficiently.

Trade Imbalance: While specific container counts are not listed, the region’s overall trade status is currently that of a net importer [Turn 10]. In 2025, Africa’s trade deficit was expected to widen to 3.4% of GDP due to subdued commodity prices and slowing global demand.

Efficiency Gains: The implementation of One-Stop Border Posts (OSBPs), such as those at Beitbridge and Nakonde, is intended to reduce the delays that “often outweigh the transit time” between ports and inland markets.

“Gaborone: The heart of Botswana’s economy—and its paradoxes.” Attribute: UN Tourism

What Sets The Study Apart

While there are global studies examining governance, workforce development, systems thinking, and unemployment independently, the STRLDi unemployment study appears to be among the first known attempts to integrate these dimensions into a single national systems framework. The study examines unemployment not merely as a labour-market issue, but as a structural output emerging from the interaction between governance systems, productive-capacity design, labour allocation patterns, aspiration systems, emotional structures, and national narratives.

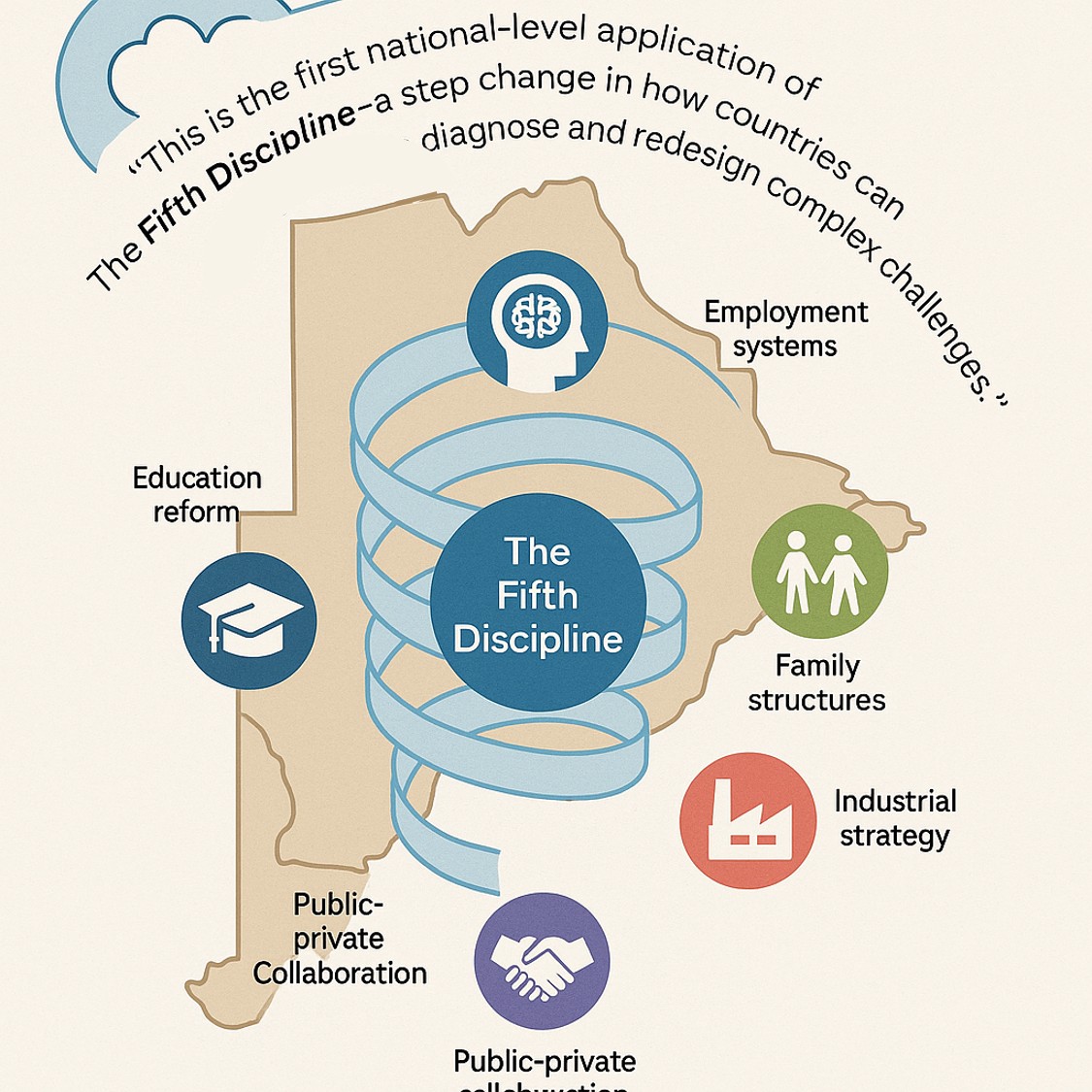

Pioneering Systems Thinking for National Transformation

This is the first study of its kind in the field of Learning Organisation, and the first known application of The Fifth Discipline on a national economic scale. It represents a breakthrough not only for Botswana, but for the global community of systems thinking practitioners, in the Senge Forrester lineage.

We are delighted to share insights into how systems thinking can be used as a research methodology—moving beyond reflection, into structured, evidence-based intervention. This work pioneers new ground for how governments, businesses, and communities can approach complex, large-scale challenges.

It aligns with Peter Senge’s long-standing call to integrate systems thinking with robust research and practical application. This approach has gained recognition within the global Society for Organizational Learning (SoL) community and highlights the urgent need for more researchers and practitioner-leaders to co-create solutions across domains.

“This is not just a study. It is a prototype for how learning, leadership, and structure can come together to solve problems that have defied generations.”

What We’re Missing Why unemployment persists despite decades of investment

A Systems View Framing unemployment as a systemic design issue, not individual failure

Why the Economy Isn’t Absorbing Labour The mismatch between GDP growth, employment, and sectoral profitability

The Circulation Crisis How money flows out of the economy, weakening internal productivity loops

From Retail-Led Growth to Production-Led Resilience Why agriculture and manufacturing must be restructured to drive sustainable employment

A Learning Milestone in Systems Thinking How this study breaks new ground in national application of The Fifth Discipline

Opening Paragraph: Setting the Puzzle

Botswana has seen five decades of investment, aid, and policy reform—but unemployment remains stubbornly high. This isn’t due to lack of effort or funding. It’s something deeper—something structural.

Section 1: What We’re Missing

“Over five decades, Botswana has attracted billions in investment and international aid. The country has built infrastructure, expanded education access, and grown GDP per capita. Yet unemployment continues to rise, and the economy feels increasingly unable to absorb the talents of its people.”

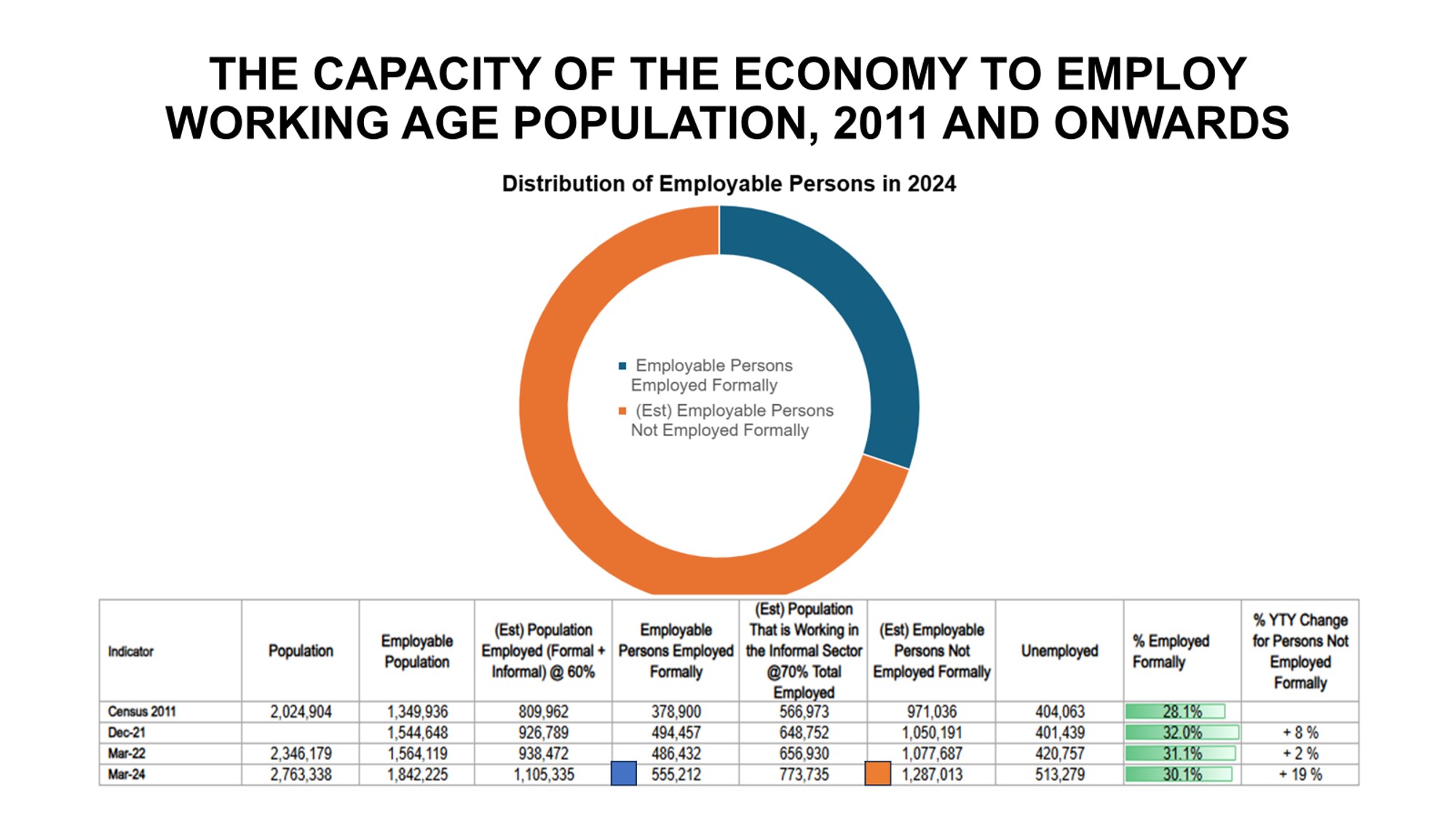

Investments to-date (1960s–Present)

Since Independence, Botswana has received an estimated USD 1.2 trillion (≈ P16 trillion) in investments, government spending, and aid. Over the same period, our population has grown from approximately 580,000 in 1966 to around 2.7 million today. This translates to roughly USD 600,000 (≈ P8 million) invested per person over five decades—excluding inflation adjustments (sources: The Guardian, Reuters, Wikipedia).

As of Q1 2024, approximately 504,738 individuals are formally employed in Botswana—defined as those holding wage or salary jobs in the formal sector (VCDA.afdb.org, Trading Economics, Botswana LMO).

To put this in context:

The average monthly wage in the formal sector is P7,149 (~USD 500) (Stats Botswana Q1 2024, ILO, Botswana LMO).

Botswana’s total labor force is estimated at 1,173,186 individuals.

Therefore, only 43% of the labor force holds formal employment.

This is clear evidence that decades of investment have not translated into shared prosperity.

Despite numerous policy interventions, unemployment in Botswana has remained persistently high. With just 43% formally employed, and an estimated 1.5 million working-age individuals, this leaves 57%—nearly 6 in 10 employable people—without access to sustainable income.

“Our challenge is not the absence of effort or policy. It is the absence of a structure that is designed to translate growth into widespread, sustainable income.”

“Formal employment absorbs less than half the country’s working-age population. And of those absorbed, most are concentrated in a handful of public sector or capital-intensive industries that don’t scale with population growth.”

“The labour market isn’t broken because people are lazy. It’s broken because it was never structurally designed to absorb everyone.”

Growth ≠ Jobs

Here is the combined graph showing:

Botswana’s GDP (in billions of BWP, left Y-axis)

Population dynamics (right Y-axis), broken down into:

Rising unemployment and non-formal employment indicate structural absorption issues

“We continue to build systems that reward GDP growth, but not labour absorption. The mismatch is systemic, not accidental.”

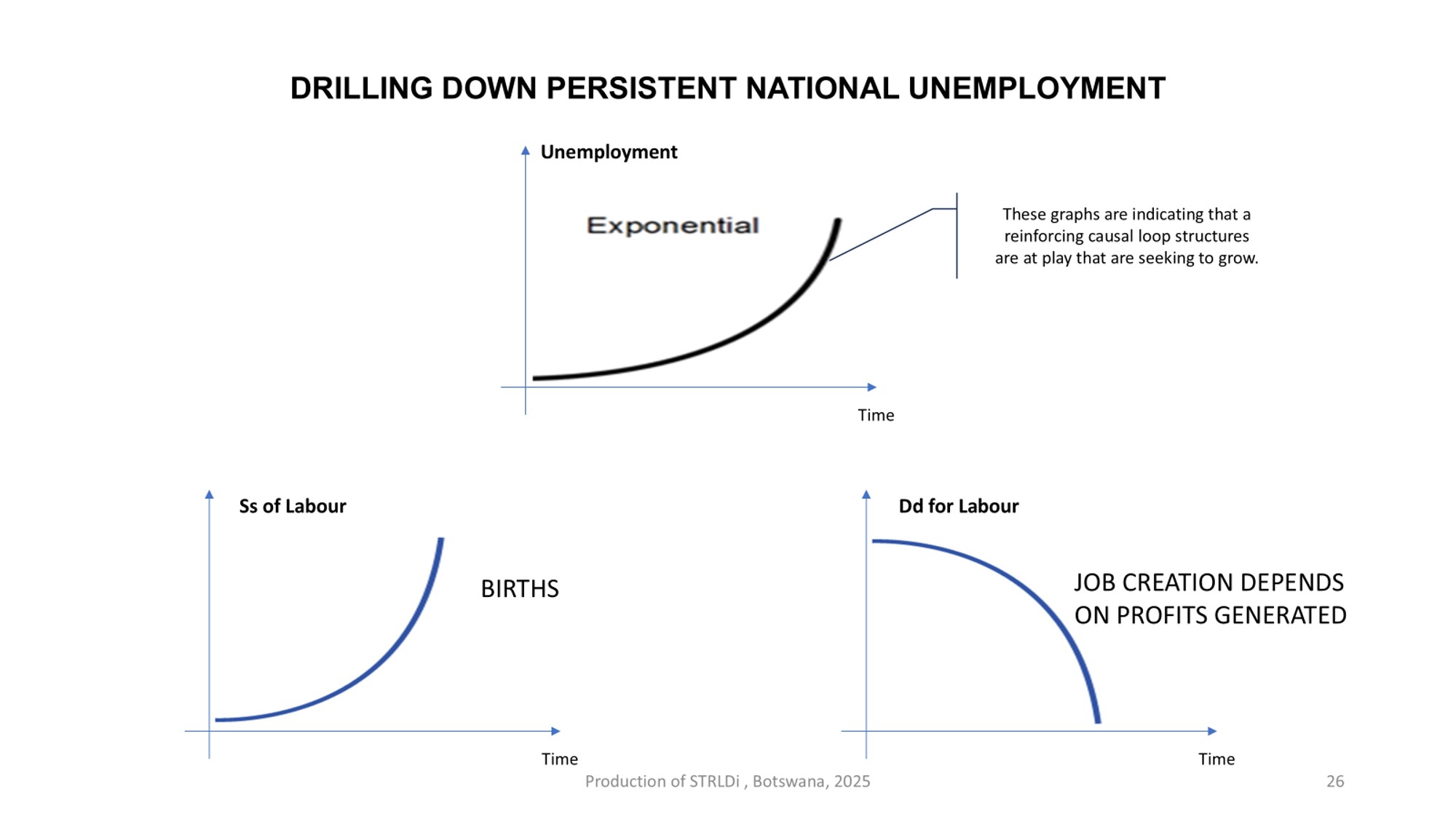

Section 2: A Systems View

“What if unemployment in Botswana isn’t simply the result of failed programmes or policy gaps? What if it is the predictable outcome of how the system is designed?” (Part 1)

The study draws on insights from Peter Senge’s The Fifth Discipline, particularly its emphasis on systems thinking—a way of seeing problems not as isolated events, but as patterns produced by structures, delays, and feedback loops.

Source: STRLDi analysis using Statistics Botswana, World Bank/ILO, and national labour data.

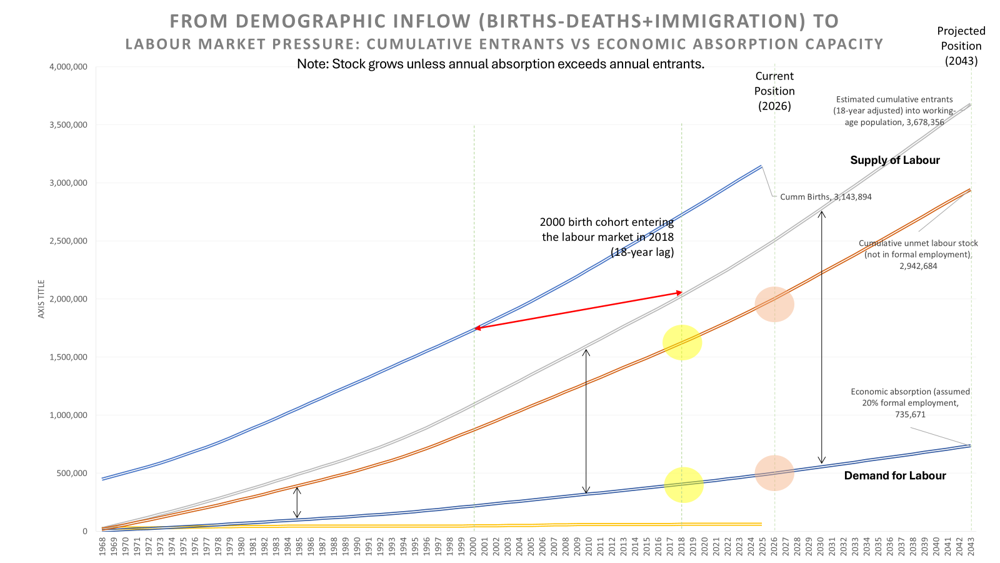

📊 From Demographic Inflow to Labour Market Pressure

This Behaviour Over Time (BOT) graph traces the structural build-up of unemployment in Botswana by comparing cumulative labour supply (driven by births, deaths, and immigration) against economic absorption capacity (formal employment).

The upper trajectory represents the supply of labour — a steadily rising curve shaped by demographic inflows. Notably, each birth cohort enters the labour market approximately 18 years later, creating a predictable and continuous increase in entrants over time. This growth persists regardless of leadership or policy cycles.

The lower trajectory reflects the demand for labour — the economy’s ability to absorb workers into formal employment. While this line also rises, it does so at a much slower pace, revealing a persistent gap between entrants and absorptive capacity.

The widening space between these two curves represents the cumulative unmet labour stock — individuals who are not absorbed into formal employment. By the current position (2026), this gap has grown significantly, and projections to 2043 show it continuing to expand if the structure remains unchanged.

A critical feature of this graph is that it shows stock accumulation, not just annual flows. Even if job creation improves in a given year, the backlog continues to grow unless annual absorption exceeds annual entrants — a threshold that has not been met.

The highlighted points along the curves draw attention to specific periods where:

Labour supply accelerates due to demographic momentum,

Absorption remains constrained, and

The system quietly compounds pressure over time.

“Systems thinking helps us move beyond symptoms. It challenges us to ask: What are the underlying structures that keep producing the same results—even when we change the players, the funding, or the policies?” (Part 1)

What becomes clear is that unemployment in Botswana is not a short-term fluctuation but a structural outcome. The pattern has remained consistent across policy shifts, economic cycles, and leadership changes — indicating that the causal structure itself is driving the behaviour.

Left unchecked, this structure will continue to steer future outcomes along the same trajectory.

The opportunity, however, lies in seeing it clearly. Once the structure is understood, the direction of the system can be deliberately changed.

The unemployment study does not treat joblessness as a standalone issue. Instead, it approaches it as a system-wide pattern—shaped by how we educate, govern, allocate capital, and design labour absorption pathways.

“We must shift from treating unemployment as a problem to be solved, to seeing it as a system to be redesigned.”

Circular traps within the system (e.g., weak education feeding low productivity)

“Unemployment persists not because of individual failures—but because of reinforcing loops built into the system.”

Section 3: Delays, Stocks, and Structures

One of the most overlooked dynamics in Botswana’s unemployment crisis is delay—the long and predictable time lag between population growth and job readiness.

“We know when children are born. We know how long it takes to educate and prepare them for the workforce. Yet national economic planning treats workforce entry as a short-term policy issue, rather than a structural inevitability.”

This is a classic stock-and-flow problem:

The stock is the growing pool of working-age individuals.

The flow—job creation—has not kept pace with this growth.

Delays between population growth and job readiness

But the challenge runs deeper. Even when new entrants are ready to work, Botswana’s economy struggles to absorb them. The missing link? The country’s capacity to scale production and market reach.

Production Constraints and Market Access

Botswana’s enterprises—particularly in manufacturing and agriculture—have not been able to consistently meet regional and international standards in quality, speed, and output volume. This is not due to lack of ambition, but to the limited readiness of the workforce to perform at scale. Even where isolated excellence exists, system-wide performance is weak.

“When firms can’t meet standards consistently, they can’t retain or expand markets. And without markets, there’s no growth. Without growth, there’s no hiring.”

This creates a self-reinforcing loop:

As a result, firms choke themselves out of opportunity—not because of external shocks, but because of internal misalignments between labour, process, and market demand.

Evidence from Sector Data

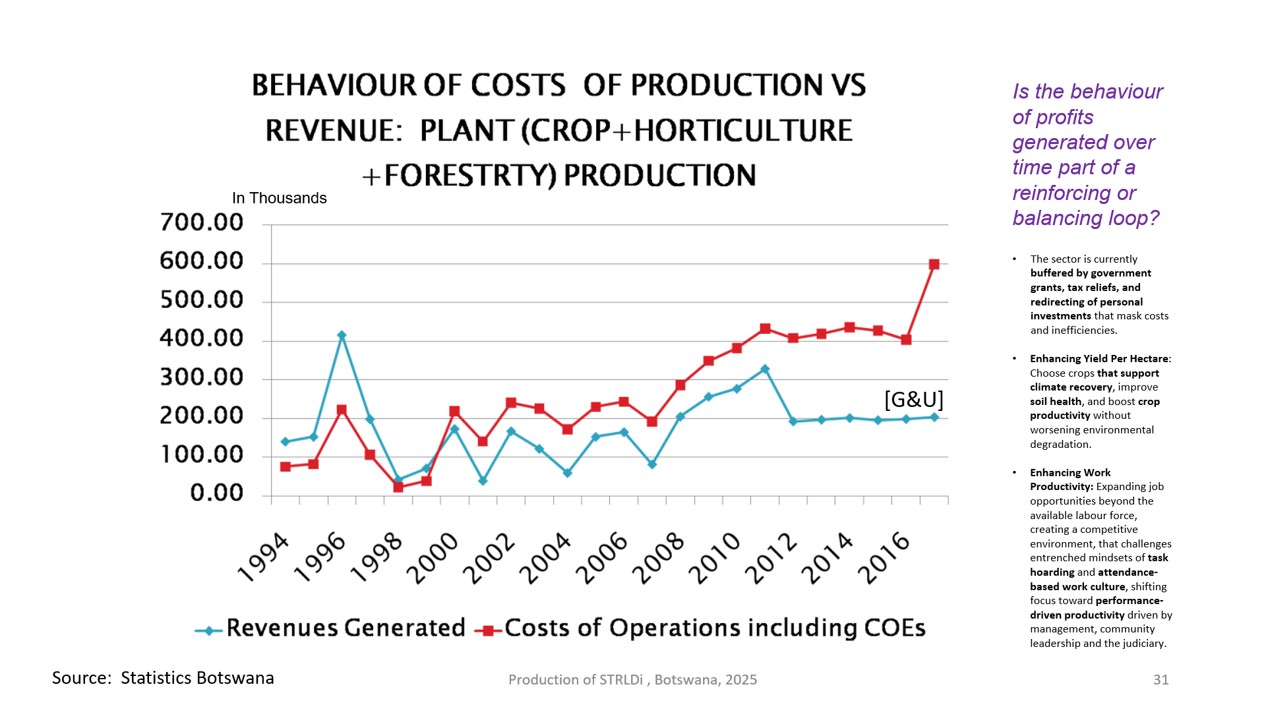

The study’s behaviour-over-time graphs show that even with investment, manufacturing and agriculture have failed to generate sustained profitability as national sectors.

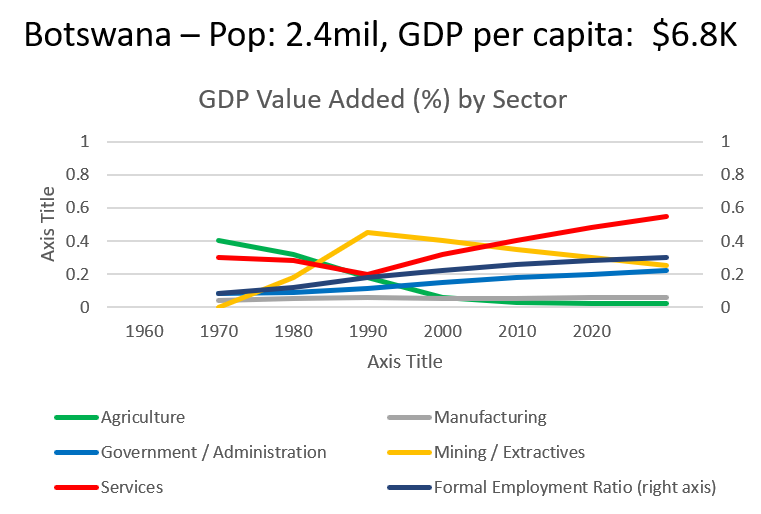

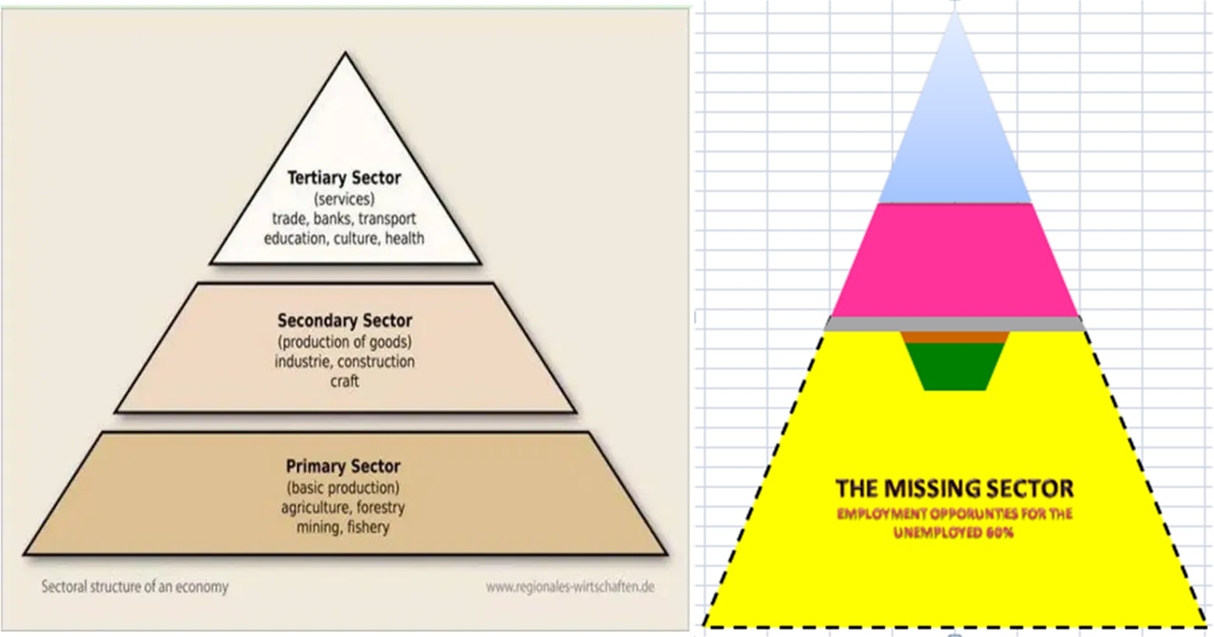

THE CAPACITY OF ECONOMIC SECTORS TO CREATE EMPLOYMENT

Since surpassing the mining sector in 2008, retail has become the leading driver of Botswana’s economy. Its continued growth reflects the rising influence of commerce, services, and consumer demand in shaping economic progress. Unlike mining, which depends on finite resources, the retail sector thrives on innovation, entrepreneurship, and the ability to respond to evolving needs. With revenues steadily outpacing costs, retail offers strong potential for job creation, business expansion, and economic resilience. Targeted investment in skills development, digital transformation, and local enterprise growth can further strengthen this vital sector.

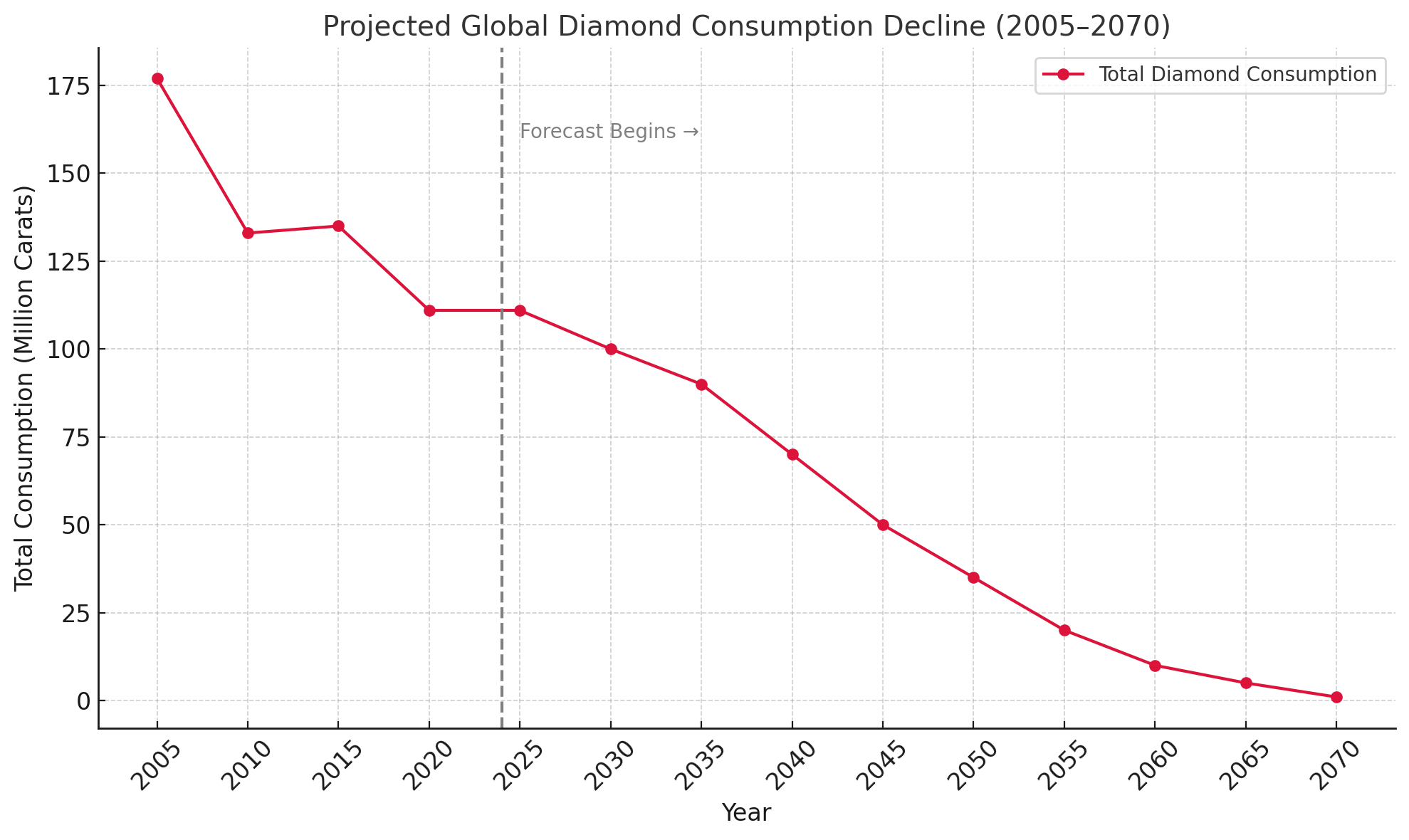

Once the backbone of Botswana’s economy, the mining sector has faced growing volatility since the 2008 global financial crisis. Revenues have fluctuated, and lab-grown diamonds are gaining ground with global consumers due to their lower cost. While a recovery remains possible as global markets improve, the sector has shown no sustained growth over the past two decades. This prolonged uncertainty underscores the urgent need for economic diversification and greater investment in industries that offer long-term stability and resilience.

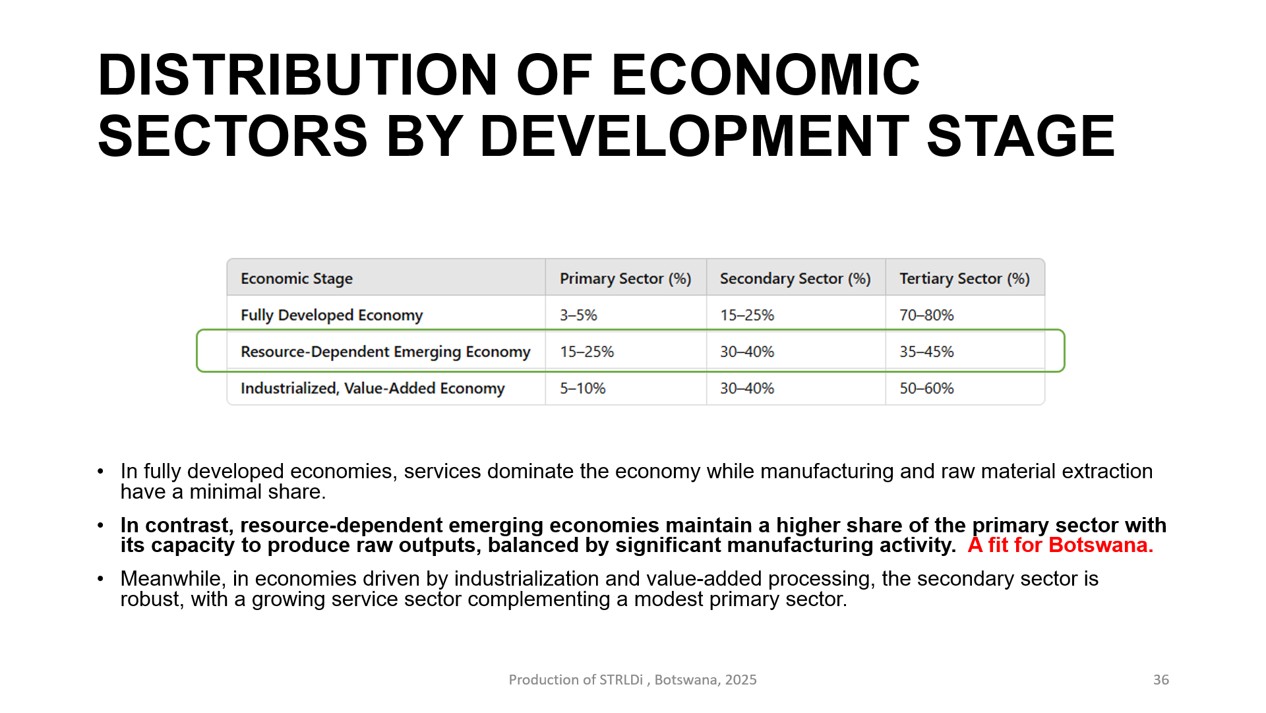

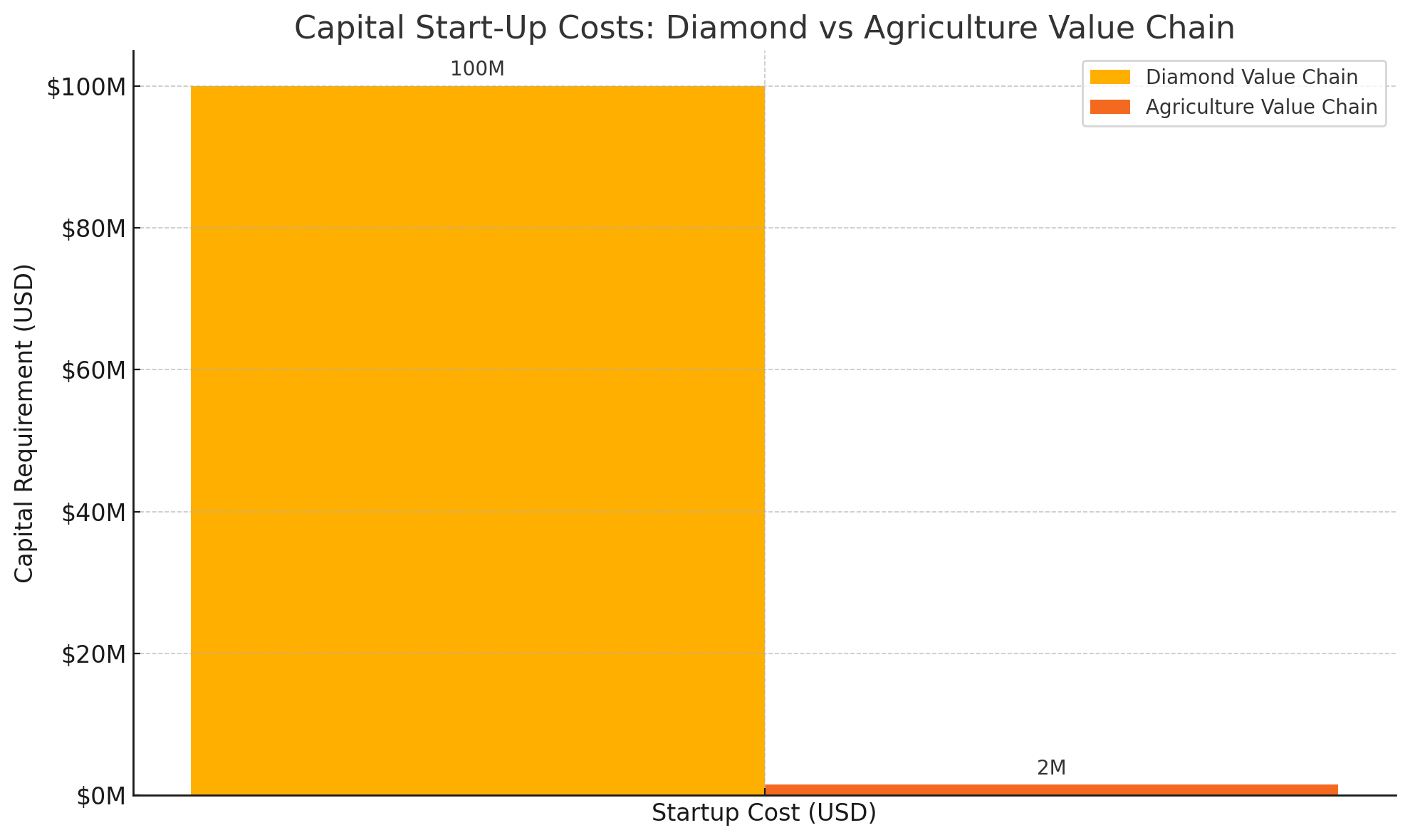

Resource-dependent emerging economies often balance raw material production with a strong manufacturing base to drive growth. Botswana, centrally located and landlocked, holds untapped potential as a regional hub for both agriculture and manufacturing, offering vital employment opportunities.

However, these sectors have struggled to take off. They contribute less than a tenth—and in some cases as little as a fiftieth—of what the retail sector generates. As a result, job creation has stalled. Agriculture and manufacturing have yet to establish profitable, scalable business models capable of supporting long-term economic growth (G&U).

To fully realize its potential, Botswana must restructure its agriculture and manufacturing sectors to ensure they are both competitive and sustainable.

A well-developed plant- and animal-based production and manufacturing sector (left diagram) lays the groundwork for regenerative, future-facing growth. It provides a strong foundation for sustainable economic development while generating and absorbing significant employment.

By contrast, extraction-based industries (right diagram) are typically capital- and technology-intensive, employing fewer people and depleting the natural resources essential for building a resilient, job-creating economy.

GROSS PRESENTATION OF THE SCALE OF THE ECONOMY. (AS OF THE LAST CENSUS YEAR IN 2011) PRESENTED BY ECONOMIC SECTORS. IT ALSO INCLUDES THE MISSING SECTORS.

IT SHOWS THE SCALE OF THE UNEMPLOYED WHEN THE FOUNDATION SECTORS ARE MISSING.

The grey, brown, and green portions represent the sizes of the manufacturing, mining, and agriculture sectors’ ability, respectively. These sectors should be readied to absorb unemployment. https://en.wikipedia.org/wiki/Botswana

The Circulation Crisis: When Value Doesn’t Flow

When Earning Isn’t Enough: The Circulation Crisis

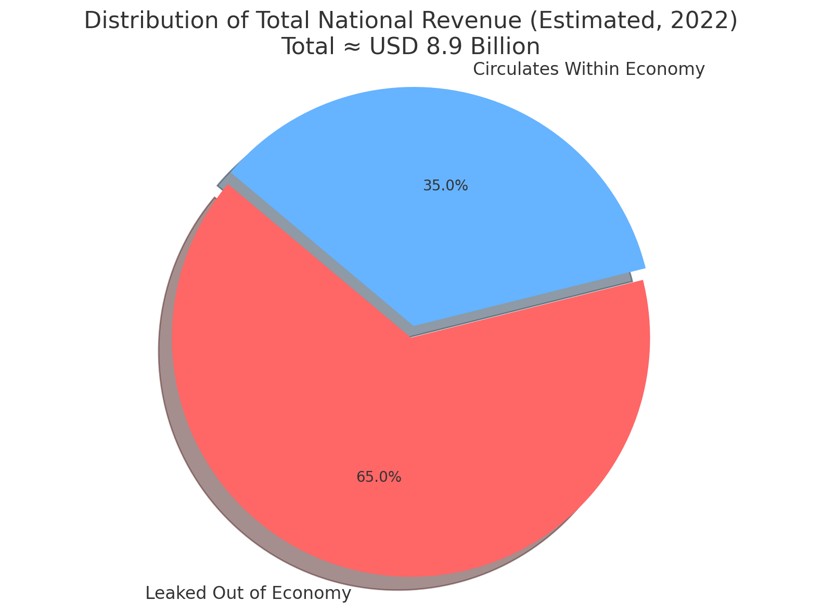

Botswana has built an impressive track record of export-led earnings and prudent fiscal management, but a deeper issue persists beneath the surface: the money we earn does not stay in the economy long enough to generate sustained impact. Instead, it exits almost as quickly as it enters—through imports, repatriated profits, external contracts, and other financial leakages. This pattern undermines the very purpose of economic growth. It’s not that Botswana doesn’t earn—it does. The problem is that those earnings don’t multiplywithin the local economy, depriving it of the fuel needed to create jobs, deepen industries, or uplift communities. This paper unpacks the scale of that leakage, where it goes, what remains, and what must be done to reverse it.

Exporting Wealth, Importing Dependency

It is a fair and data-backed observation that a substantial share of the income Botswana earns—whether through exports, government revenue, or trade—does not stay within the economy but instead exits rapidly. This dynamic is particularly evident in years like 2022, when Botswana exported approximately USD 8.9 billion worth of goods, yet spent about USD 8.7 billion on imports. That means nearly every pula earned through international trade was matched by a pula spent abroad. The result is a system where revenues generated through diamonds and other exports flow out just as quickly via imported fuel, machinery, vehicles, food, and services, with little absorption into domestic value chains. Without robust processing, manufacturing, or reinvestment capacity, the economy behaves like a conduit rather than a container—passing wealth through without compounding its benefits locally.

How Much Leaves, How Little Stays

In estimating the leakage, if we treat total exports (≈ USD 8.9 billion) as a proxy for total revenue, and combine import spending with factors like profit repatriation, external contract payments, and debt service, a conservative estimate suggests that at least 60–80% of this national income leaves the country. That means only 20–40% of what Botswana earns circulates internally—supporting government wages, local consumption, and limited domestic procurement. In 2022, for example, government revenue stood around USD 5.5 billion, while import bills were higher still at USD 8.7 billion—making imports roughly 158% of revenue. This points to a structural imbalance where even sovereign income is insufficient to retain wealth domestically.

The Need to Build Domestic Multipliers

What little money remains is spent primarily on public salaries, social services, and recurring operational costs, which in turn often rely on imported inputs—thereby creating additional layers of leakage. Without strengthening Botswana’s domestic production capacity—especially in manufacturing, agriculture processing, and infrastructure development—these funds will continue to create jobs and incomes elsewhere, not at home. The weak local value chain not only limits domestic job creation but also increases vulnerability to external price shocks and supply disruptions. Unless this economic architecture is reshaped to prioritize internal circulation and value capture, Botswana may continue to earn big but circulate little—leaving a growing population without the employment or enterprise opportunities it deserves.

The result? Botswana’s economic engine spins but does not pull. Resources move at the top, but do not multiply across the broader economy.

“We earn, but we don’t multiply. We produce, but we don’t distribute. This is how an economy grows on paper but feels stuck in practice.”

Section 4: What the Study Did

This study set out not merely to document unemployment trends in Botswana, but to reveal the underlying structures that continue to produce them—despite well-intentioned policies, funding, and reform efforts. It applies systems thinking, drawn from The Fifth Discipline by Peter Senge, to diagnose the national economy as a living system—one that has not been designed to absorb its people into meaningful, productive livelihoods.

The study using 20-year data:

Tracked the disconnect between population growth and employment absorption

Identified sector-level profitability stagnation, particularly in agriculture and manufacturing

Mapped the structural traps and feedback loops reinforcing unemployment and low productivity

Highlighted the circulation crisis—how value generated fails to move across the economy in a way that multiplies opportunity

“The problem isn’t a lack of effort—it’s that we’re working inside a system that was never designed to deliver the outcomes we now expect.”

At its core, the study surfaces three persistent systemic failures:

The Absorption Gap: There is no built-in pathway to absorb the growing workforce into formal, productive sectors.

The Productivity Trap: Key sectors remain underperforming, not from lack of investment, but from workforce misalignment and poor process standards.

The Circulation Breakdown: Value accumulates in isolated areas without circulating into broader economic and employment growth.

Using systems thinking tools—such as feedback loops, time delays, stock-flow structures, and archetypal traps—the study identifies leverage points that could reverse these patterns:

Aligning education, training, and production

Restructuring sectors to reinvest and scale

Redesigning governance for flow, not fragmentation

Here is the closing paragraph for Part 1, crafted to bring the post to a thoughtful and anticipatory conclusion, while inviting readers forward into Part 2:

Conclusion: Preparing for the Deep Dive Ahead in Part 2

Botswana’s persistent unemployment is not the result of any single actor or decision. It is the outcome of a system whose design has not kept pace with its people. This study reveals that until job creation is structurally embedded—until sectors are rebuilt for absorption, productivity, and flow—the frustration across government, private sector, and households will continue.

But there is a path forward.

Through the lens of systems thinking, we begin to see where leverage lies—not just in programmes or reforms, but in the very architecture of how our economy functions. In Part 2, we examine the specific feedback loops, social disruptions, and sectoral misalignments that reinforce the current state—and explore how these can be shifted.

“The goal is not to fix the old system. It is to redesign the economy so that people—and their potential—are no longer left out of the future.”

Introduction to Part 2

Click here for Part 2 of the article. It covers the next:

Yes, we do. Here’s the refined write-up for the section titled:

🎓 A Learning Milestone in Systems Thinking

How this study breaks new ground in national application of The Fifth Discipline

This is the first study of its kind in the field of Learning Organisation. It marks the first large-scale application of Peter Senge’s The Fifth Discipline to a national issue—persistent unemployment—and does so using a full systems diagnosis. This milestone represents not just a personal achievement, but a breakthrough for the global community of systems thinking practitioners.

It demonstrates that the discipline of Systems Thinking can be rigorously applied beyond organizations—into the complex, cross-sectoral domain of national development. For those working on public policy, economic transformation, and institutional renewal, this work offers a new, structured framework for addressing systemic stagnation.

The study aligns with the direction advocated by Dr. Senge and the global Society for Organizational Learning (SoL): pairing systems thinking with robust research methodology. It also underscores the importance of not isolating systems thinking as a “soft” or intuitive practice, but grounding it in structured diagnosis, modelling, and evidence-based design.

🔖 Pull Quote

“This is the first national-level application of The Fifth Discipline—a step change in how countries can diagnose and redesign complex challenges.”

We welcome the opportunity to engage with researchers, educators, governments, and private sector partners who want to better understand this methodology—and consider how it might be adapted to other pressing national or regional challenges. The study offers a replicable approach for countries confronting economic exclusion, sectoral imbalance, or policy fragmentation.

🔹 Technical Appendix Note

Note on Methodology and Assumptions

This Behaviour Over Time (BOT) graph is constructed using cumulative estimates of labour market entrants derived from demographic inflows (births adjusted for deaths and net migration), with an assumed 18-year lag to represent entry into the working-age population.

In the absence of complete year-by-year data, intervening annual variations were smoothed, and estimates were applied in a manner that ensures cumulative alignment with known reference points, including the observed labour market position in 2025–2026.

The demand curve reflects formal employment absorption capacity, based on available employment data and projected growth trends.

The resulting gap represents the cumulative unmet labour stock — individuals not absorbed into formal employment. It is important to note that this is a stock accumulation model, meaning that unless annual job creation exceeds annual entrants, the gap will continue to widen over time.

This model is not intended as a precise yearly forecast, but as a structural representation of system behaviour, allowing for identification of underlying causal dynamics rather than short-term fluctuations.

🔎 Source

Author’s analysis (STRLDi), based on compiled data from:

Statistics Botswana – Population, Labour Force, and Employment Data

World Bank / ILO – Labour market and demographic benchmarks

Ministry of Finance & National Planning (Botswana) – Budget and economic reports

HRDC (Human Resource Development Council) – Labour and skills data inputs

Model constructed using cumulative demographic inflow (births – deaths + net migration) with an 18-year labour market entry lag, and estimated formal employment absorption capacity.

“Strategic Reflection: Toward a Regenerative Botswana Economy”

What if the real challenge in governance isn’t corruption or inefficiency? Instead, it may be the absence of a shared, cross-sector system. Such a system can hold a vision over time.

Around the world, the systems we’ve inherited were designed for different eras. Some were from the colonial era, and others from the industrial era. Few are built to match the complexity, interdependence, and generative potential of today’s global economy.

And in Africa, our response to this gap is long overdue.

So, what might such a system look like?

The method of sustaining employment through government tenders, grants, and extractive economies for export is reaching its limit. This approach has been used across the public, private, and informal sectors. Tax revenues generated from foreign investments are redistributed into health, education, security, and infrastructure. This model, while protective and supportive, lacks growth in high-value (90%+) productive activities by its population in agriculture. This is needed in processing and manufacturing. Such growth is essential for long-term economic resilience and creating national wealth.

If Botswana is serious about diversifying its economy and building enduring, generational wealth, this model must be reformed, i.e. from a redistributive to regenerative economy.

Any wealth accumulation by the nation before taking this foundational step risks being premature. It could be unjustifiable and border on a misappropriation of public trust and resources.

In this transformation, it is imperative that the government’s socialist functions are gradually reduced. These functions include providing direct support to youth, women, and the elderly. In fact, these functions will fall away naturally as families stabilize. A generative, production-based economic model will enable the core family unit to re-assume responsibility for their well-being.

Dividing these groups for short-term political gain may yield momentary advantage, but it results in long-term economic fragmentation and loss.

What then is a structured governance workforce distribution model for Botswana, based on a projected population of 5–8 million (from today’s 2.5 million) over the next 30 years, with a per capita wage of P20,000 (cf to today’s P1,600) and a GDP of $60–100 billion (today’s $20 billion). The focus will be on recommended private vs. public sector workforce shares and a detailed breakdown by ministry.

This post presents a structured overview of Botswana’s current governance architecture. It comprises Ministries, Parastatals, and formal Public-Private or Community-Inclusive Structures. All of these are currently funded through the government payroll. Building on this foundation, the report then introduces a proposed governance body. This body is designed to lead Botswana into a future anchored in regenerative, value-creating economic transformation.

POST ROADMAP:

Given the post’s depth and evolving focus, we are providing a simple outline that will help readers stay oriented.

In This Post – Recalling What Governance Meant – Seeing What the World Is Showing Us – Why Africa’s Frameworks Must Evolve – Rethinking Our National Structure – Lessons from the DM Model – The Next Step Forward

🧩 Inquiry Roadmap – Guiding Questions Behind the Essay

Here’s a list of guiding questions used in the development of the full essay.

The essay is titled “When the World Speaks – Governance BW”. This list acts as a roadmap of inquiry. It traces the intellectual journey from challenge recognition to structural diagnosis. It continues to the design of a proposed national governance framework. Finally, it leads to the integration of policy learning from the DM model.

These questions were raised across multiple conversations over the past 2–3 weeks (with DM model-specific queries toward the latter part). Use them to orient yourself as the reader at the start of the essay. They invite you to walk the same arc of discovery.

🌍 SYSTEMIC PATTERNS & CONTEXTUAL FRAMING

Why do we continue to experience policy and governance failures even under capable leadership?

Are we suffering from individual incompetence, or structural design limitations?

What do governance collapses in wealthy nations (like the US, UK, France) reveal about deeper, global system failures?

What invisible assumptions and outdated structures still drive governance decisions in post-colonial African countries?

🧠 SYSTEMS THINKING & ARCHETYPES

How do systems archetypes (e.g., Growth & Underinvestment, Shifting the Burden) explain the persistence of unemployment and underdevelopment?

Why do investments in key sectors fail to produce long-term transformation?

What is the cost of failing to reinvest into production systems (e.g., agriculture, STEM, trade readiness)?

How do beliefs around status, education, and short-term relief distort structural priorities?

🧱 GOVERNANCE DESIGN & VISION

What type of governance structure would allow ministries and the private sector to jointly lead national transformation?

How can we design a governance body that transcends political cycles and operates with long-term, technocratic continuity?

Should national strategic leadership be led 65% by private sector actors?

How do we retain political legitimacy while introducing structural discipline?

🧩 STRUCTURAL ROLES & DIFFERENTIATION

What is the role of the new governance council versus ministries or existing agencies?

How do Deputy PMs for Growth and Stabilisation unlock this structure?

What kind of regional integration bodies (e.g., value chain councils, export readiness platforms) need to be embedded?

How does this proposed structure compare with traditional silos or “super-ministries”?

🛠️ DEVELOPMENT MANAGER MODEL – DEEP DIVE

These questions came up during the second phase (last week). They shaped the integration of DM lessons into the governance proposal.

What was the Development Manager (DM) model in Botswana originally responding to?

What failures or inefficiencies in pre-DM structures made the model necessary?

Did the DM model reduce cost overruns, delays, and patronage as intended?

Who benefited most and least from the DM model?

What scope changes were introduced by ministries, and what penalties (if any) were imposed?

Did the DM model incentivize good planning, or shield poor performance?

How do we distinguish the DM’s role from the proposed national governance framework?

What reforms are needed to align DM performance with strategic national goals?

⚖️ REFORM & ACCOUNTABILITY MECHANISMS

Should ministries that trigger scope changes bear financial responsibility (variation cost attribution)?

How can we cap government-backed project budgets, forcing external sourcing for overruns?

What role can an independent Variation Review Panel play in containing costs?

Should a Ministry Performance Ledger be introduced to publicly track project delivery?

What systems of consequences and learning loops are needed to sustain structural integrity?

🧩 STRUCTURAL INTERFACE: DM MODEL & GOVERNANCE FRAMEWORK

If the governance framework doesn’t manage infrastructure directly, what does it do?

How do the governance body and the DM model complement each other?

Who governs the DM model, and what strategic scaffolding does the governance structure provide?

Why is it important that private sector manage private-sector-oriented delivery structures?

🌱 NARRATIVE & IDENTITY

What kind of national identity does this new governance structure invite us to build?

How can we communicate this proposal as a values-driven, systems-grounded national renewal — rather than a technocratic power shift?

Reader’s Roadmap: What This Essay Asks and Answers

This essay was not written in one sitting. It was shaped through weeks of inquiry, questioning, and collaborative reflection. Below is a guide to the key questions that shaped its development. You are invited to walk the same arc of discovery.

Why do governance systems fail — even in capable nations?

What outdated structures still constrain post-colonial governance?

Can systemic patterns explain persistent underdevelopment in Botswana?

What does a reimagined governance model look like — and who leads it?

What lessons can we learn from Botswana’s own Development Manager model?

What reforms are needed to build accountability, investment readiness, and national pride into our governance design?

How can we collectively build a regenerative, globally integrated economic engine — rooted in systems thinking and national identity?

🏛️ Ministries

Below are the key Ministries under the central government (Cabinet formed November 2024–March 2025):

Office of the President & State President (presidential affairs, communications, ethics/integrity, disaster, audit, electoral, etc.) (gov.bw, finance.gov.bw)

Botswana Geoscience Institute, Innovation Hub, Accountancy College, Energy Regulatory Authority, Examination Council, National Development Bank (NDB) (gov.bw, en.wikipedia.org, gov.bw, imf.org, en.wikipedia.org)

These parastatals receive government payroll support and are overseen via shareholder compacts monitored primarily by the Public Enterprises Evaluation and Privatization Agency (PEEPA) under the Ministry of Finance (imf.org).

🔗 Public–Private–Community Governance Structures

PPP Unit (Ministry of Finance & Economic Development)

A dedicated PPP Unit, formed under the 2009 PPP Policy/Implementation Framework, coordinates private sector involvement in infrastructure/social projects; it approves and manages project-level PPP committees (blogs.worldbank.org).

PPP Project Committees

Established for each PPP initiative, these include government, private sector partners, and sometimes community representatives, under contractual performance frameworks (blogs.worldbank.org).

Local Government Councils (e.g., Gaborone City Council)

Councils include elected community councillors plus municipal staff; they collaborate with parastatals like Water Utilities Corporation and BPC, and run public services such as clinics and schools (en.wikipedia.org).

Ministry Offices with Community Functions

e.g., Ministry for State President includes Offices like coordinating disability services, disaster management, district administration, ethics, corruption prevention and public communications (gov.bw).

📌 Summary Table

Type

Examples

Includes Private/Community?

Ministries

Listed above

Mostly public-sector, some incorporate District admin

Parastatals

~62 SOEs (BPC, BoFiNet, NDB, etc.)

State-owned, commercial services

PPP Governance Structures

PPP Unit, PPP Committees

Formalized private-sector partnerships

Local Councils

Gaborone City Council, other municipal councils

Elected community leaders, parastatal coordination

✅ Conclusion

Botswana’s government payroll landscape spans from traditional ministries and SOEs to community-inclusive municipal councils and formal public–private partnership structures. The PPP Unit and Project Committees primarily connect the government to private-sector collaboration. Local Councils provide community‑led governance below the national level.

WHAT THE WORLD IS SHOWING US

Which countries lead in the top three by volume produced per capita for manufacturing?

Here are the top three countries by manufacturing value added per capita, based on the most recent data (UNECE):

🏅 Top Three (Value Added in USD per Capita)

Liechtenstein: ~ 63,000 USD

Switzerland: ~ 19,000 USD

Norway: ~ 5,200 USD

These figures refer to manufacturing value added per person in each country, not total output (w3.unece.org).

🧭 Context & Interpretation

While nations like China, United States, and Germany dominate in total manufacturing output, per capita measures offer a different perspective. These measures highlight smaller economies with high-value industrial sectors. These sectors are often in specialized and capital-intensive manufacturing.

For example, Liechtenstein tops the list due to its robust precision manufacturing industry combined with a small population (ft.com).

🔍 Why Does This Matter?

Per capita metrics normalize for population and reveal how much manufacturing “productivity” each person contributes.

High per capita values often signal economies focused on advanced, high-tech, or luxury manufacturing, rather than large-scale mass production.

🆚 Compare with Total Output

For comparison, consider these total manufacturing leaders in absolute terms (2023):

But when adjusted per person, countries like Liechtenstein, Switzerland, and Norway emerge as the clear leaders.

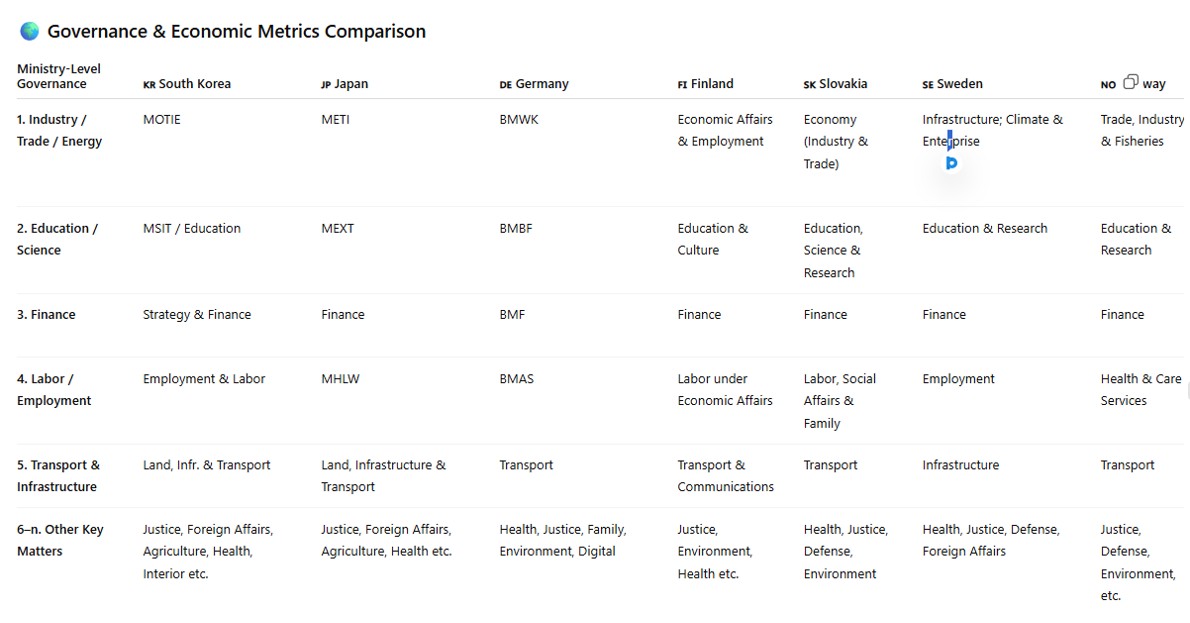

How Governance Structures Shape Citizen Participation in the Manufacturing Economy

We first examined the governance structures (MDAs—communities, education, raw material extraction, manufacturing, retail, and trade) of six countries. We looked at whether or not they have actively promoted economic growth. Our focus was on how gains from manufacturing are distributed directly to citizens as earned wages. This distribution is not in the form of aid or grants.

This distinction is critical. It is how countries ensure their populations meaningfully participate in the manufacturing economy. This participation spans from early health and education through adulthood. It includes ongoing skills and reskilling efforts.

✅ Summary Table

Country

Vocational Pathway

Governance Model

Direct Salary Focus?

Switzerland

Apprenticeship + school

Federal/cantonal + industry tripartite

✅ Yes—earn while learning

Norway

VET upper-secondary

Municipal, counties + NAV coordination

✅ Yes—block funding, wages

Germany

Dual VET

Federal/state + firms

✅ Yes—firm-paid apprenticeships

Liechtenstein

Swiss-style VET

Cantonal/federal + industry

✅ Yes

United States

Apprenticeships & institutes

Federal + industry networks

✅ Yes—paid programs

China

VET via SOEs

Central/local ministries

❌ Unclear—welfare still key

🌍 Countries Ensuring Direct Gains in Manufacturing

Switzerland, Norway, Germany, Liechtenstein, and parts of the United States have governance systems that integrate education, training, and manufacturing. These systems ensure individuals earn wages through direct employment or paid apprenticeships.

🚫 Lagging Model – China

China heavily invests in industrial capacity. However, the pathway from training to individual wage-earning in manufacturing is less clearly guaranteed. State support and welfare still play significant roles.

⚙️ Key Mechanisms Across Successful Models

Dual VET / Apprenticeships: Firms partner with states to employ trainees from mid-education.

Governance Oversight: Multi-level collaboration—government, industry, and education bodies.

Wage Incentives: Apprentices earn living wages; firms receive support tied to wage levels.